"Talk is cheap. Show me the code."

— Linus Torvalds, popularised in the film The Social Network (2010)

The previous chapter laid out the what and the why of the

quantitative toolkit. This chapter is the how — the Python

foundations that turn the equations of Chapter 2 into pipelines you

can actually run, refit, and ship. We start with data processing

using Polars DataFrames, then move to visualization for exploratory

analysis and model interpretation. Finally, we cover the transition

to NumPy arrays and PyTorch tensors for machine learning, along with

time-series libraries that streamline forecasting workflows.

The progression follows a natural workflow: process data

(Section 03-01) → visualize patterns (Section 03-02) → convert

to arrays/tensors (Section 03-03) → use specialized libraries

(Sections 03-04 and 03-05).

Contents

DataFrames with Polars — efficient data

processing with expression-based operations, time-series patterns,

and lazy evaluation.

Time-Series Forecasting with sktime —

splitters, evaluators, and the unified forecasting interface that

makes Chapter 4's baselines portable.

DataFrames with Polars

DataFrames are the cornerstone of financial data analysis. Whether you're building forecasting models, computing risk metrics, or preparing features for machine learning, you'll spend most of your time manipulating tabular data. This chapter introduces Polars—a DataFrame library designed for the scale and complexity of modern financial AI systems.

Why Polars for Finance AI?

Financial data presents unique challenges: you work with cross-asset panels spanning thousands of tickers, time-series operations that must respect calendar boundaries, and sparse event data (earnings, dividends, corporate actions) that must align precisely with price data. Traditional DataFrame libraries struggle with these patterns, forcing you to write slow loops or drop into low-level code.

Polars solves this by combining familiar DataFrame ergonomics with an Apache Arrow memory layout, vectorized expressions, multi-threaded execution, and a query optimizer that fuses operations into efficient pipelines. As a result, You can handle large cross-asset panels, compute rolling statistics across thousands of time series, and join sparse events to dense price data—all without writing bespoke C++ or sacrificing code readability.

Learning Polars as a Pattern Language

Rather than treating Polars as just another DataFrame library, we'll approach it as a pattern language for financial workflows. Each example in this section introduces reusable idioms that solve common finance problems:

Per-ticker operations: Computing returns, rolling statistics, and lags for each asset independently

Calendar-aware resampling: Aggregating daily data to monthly or quarterly buckets while respecting trading calendars

Sparse event joins: Aligning dividends, earnings, and other events with price data without look-ahead bias

Lazy pipeline templates: Building efficient feature engineering pipelines that scale to large datasets

These patterns appear throughout the book—in forecasting models (Chapter 4), factor construction and dynamic modeling (Chapter 6), and agent workflows (Chapter 8).

Expressions

One of the key features in Polars is expression-based execution. Traditional pandas DataFrames use an imperative pattern where you modify the DataFrame step-by-step. Polars uses a declarative, expression-based approach that feels like writing SQL queries.

Pandas (Imperative Pattern):

import pandas as pd# Each operation modifies the DataFrame in placedf['Return'] = df['Close'] / df['Close'].shift(1) - 1df['ReturnZ'] = (df['Return'] - df['Return'].mean()) / df['Return'].std()df = df[df['Volume'] > 1000000] # Filter modifies DataFrame

Polars (Expression-Based Pattern):

import polars as pl# All operations are expressions that compose togetherdf = df.with_columns([ ((pl.col("Close") / pl.col("Close").shift(1)) - 1).alias("Return"), ((pl.col("Return") - pl.col("Return").mean()) / pl.col("Return").std()).alias("ReturnZ")]).filter(pl.col("Volume") > 1_000_000)

Why Expressions Are SQL-Friendly and Beneficial:

Query Optimization: Polars can see your entire pipeline before execution, enabling optimizations like predicate pushdown, projection pruning, and operator fusion. The query optimizer rearranges operations for efficiency.

Readability: Expressions read like mathematical formulas or SQL queries, making complex transformations easier to understand and maintain.

Composability: Expressions can be combined, reused, and nested without side effects. You can build complex pipelines from simple building blocks.

Lazy Evaluation: Combined with .lazy(), expressions enable deferred execution where Polars optimizes the entire query before running it—critical for large financial datasets.

String Operations with .str Accessor:

Polars provides a .str accessor for string operations, similar to pandas but optimized:

# String operations on ticker symbolsdf = df.with_columns([ pl.col("Ticker").str.to_uppercase().alias("TickerUpper"), pl.col("Ticker").str.slice(0, 3).alias("TickerPrefix"), pl.col("Ticker").str.contains("ETF").alias("IsETF"), pl.col("Ticker").str.replace(" ", "-").alias("TickerNormalized"),])# Extract patterns (e.g., extract exchange from ticker format "AAPL:NASDAQ")df = df.with_columns([ pl.col("Ticker").str.split(":").list.get(1).alias("Exchange")])

Finance Use Case: Expression-based execution is especially powerful for financial workflows because:

Feature engineering often involves many chained transformations (returns → rolling stats → normalization)

Lazy evaluation lets you build entire pipelines that only execute when needed, reducing memory usage

Query optimization automatically handles common patterns like "filter early, select late" for better performance

Time Processing

Another unique characteristic of Polars is its powerful time-series processing capabilities. Financial data is inherently temporal, and Polars provides specialized functions for calendar-aware operations, rolling windows, date extraction, and time-based joins—all critical for avoiding look-ahead bias and respecting trading calendars.

1. group_by_dynamic: Calendar-Aware Grouping

Unlike fixed-window operations, group_by_dynamic respects actual calendar boundaries (months, quarters, weeks), which is essential for aligning with reporting periods and trading calendars.

Why this matters: Calendar months have different numbers of trading days. Fixed windows (e.g., "30 days") would misalign with reporting periods. group_by_dynamic ensures your aggregations align with actual calendar boundaries.

2. rolling: Fixed-Window Statistics

Rolling windows compute statistics over a fixed number of periods, essential for technical indicators and short-term features.

# Rolling statistics per tickerfeatures = prices.with_columns([ # 20-day moving average pl.col("Close").rolling_mean(20).over("Ticker").alias("MA20"), # 20-day rolling volatility pl.col("Return").rolling_std(20).over("Ticker").alias("Vol20"), # 10-day rolling high (for breakout detection) pl.col("Close").rolling_max(10).over("Ticker").alias("High10"),])

Finance use case: Volatility targeting, momentum signals, and technical indicators all rely on rolling windows. The .over("Ticker") ensures each asset's time series is processed independently.

Note: The first 9 rows show null for rolling statistics because a 10-period window requires at least 10 previous values. This is expected behavior—rolling windows need sufficient history before producing values.

3. dt Accessor: Date/Time Extraction

Extract calendar components for grouping, filtering, and feature engineering. This requires datasets with actual Date columns (like prices_daily.csv):

# Load data with Date column (e.g., prices_daily.csv)prices = pl.read_csv("data/prices_daily.csv", try_parse_dates=True)# Extract calendar componentsprices = prices.with_columns([ pl.col("Date").dt.year().alias("Year"), pl.col("Date").dt.quarter().alias("Quarter"), pl.col("Date").dt.month().alias("Month"), pl.col("Date").dt.weekday().alias("Weekday"), # 1=Monday, 7=Sunday pl.col("Date").dt.strftime("%Y-%m").alias("YearMonth"),])# Filter by fiscal periodsq4_data = prices.filter(pl.col("Date").dt.quarter() == 4)

Finance use case: Calendar effects (month-end, quarter-end patterns), fiscal period alignment, and seasonal feature engineering.

Filtering by date ranges: Use explicit date objects to stay calendar-aware. Unlike integer indexing, this respects actual calendar boundaries. This requires datasets with actual Date columns:

from polars import date# Load data with Date column (e.g., prices_daily.csv)prices = pl.read_csv("data/prices_daily.csv", try_parse_dates=True)# Filter recent data (e.g., for backtesting recent models)recent = prices.filter(pl.col("Date") >= date(2020, 1, 1))# Filter a specific historical period (e.g., a market cycle)past_cycle = prices.filter( pl.col("Date").is_between(date(2018, 1, 1), date(2020, 12, 31)))

Why calendar-aware matters: Financial contracts, reporting periods, and trading calendars depend on actual dates, not row counts. Using explicit dates prevents bugs when data has gaps (holidays, weekends, delistings).

4. join_asof: Time-Based Joins Without Look-Ahead Bias

Align sparse events (earnings, dividends) with price data using the most recent event available at each point in time—critical for avoiding look-ahead bias. This requires datasets with actual Date columns:

# Load data with Date columnsprices = pl.read_csv("data/prices_daily.csv", try_parse_dates=True)earnings = pl.read_csv("data/earnings.csv", try_parse_dates=True)# Join earnings announcements to prices (only use info available at that time)prices_with_earnings = ( prices.sort("Date") .join_asof( earnings.sort("AnnouncementDate"), left_on="Date", right_on="AnnouncementDate", by="Ticker", strategy="backward", # Use most recent earnings before/on this date tolerance=pl.duration(days=30), # Only match within 30 days ))

Why strategy="backward" matters: This ensures you only use events that occurred on or before the trading date. Using strategy="forward" would be look-ahead bias—using future information in your model.

Finance use case: Aligning earnings announcements, analyst upgrades, corporate actions, and other events with price data while maintaining temporal integrity.

Combining Time Operations:

These operations often work together in financial workflows:

# Build monthly features with rolling statisticsmonthly_features = ( prices.sort(["Ticker", "Date"]) .with_columns([ # Rolling features pl.col("Return").rolling_mean(20).over("Ticker").alias("MA20"), pl.col("Return").rolling_std(20).over("Ticker").alias("Vol20"), # Calendar features pl.col("Date").dt.quarter().alias("Quarter"), ]) .group_by_dynamic("Date", every="1mo", group_by="Ticker") .agg([ pl.col("MA20").last().alias("MonthMA20"), pl.col("Vol20").mean().alias("MonthVol20"), ]))

These time-series operations appear throughout the book—in forecasting models (Chapter 4), backtesting workflows, and factor construction (Chapter 6).

Schema Setup

You can start by installing Polars package using your preferred package manager:

pip install polars# oruv add polars

All examples in this book use a consistent set of CSV files that represent typical financial data you'll encounter in real workflows. Understanding this structure helps you see how Polars patterns apply to your own data.

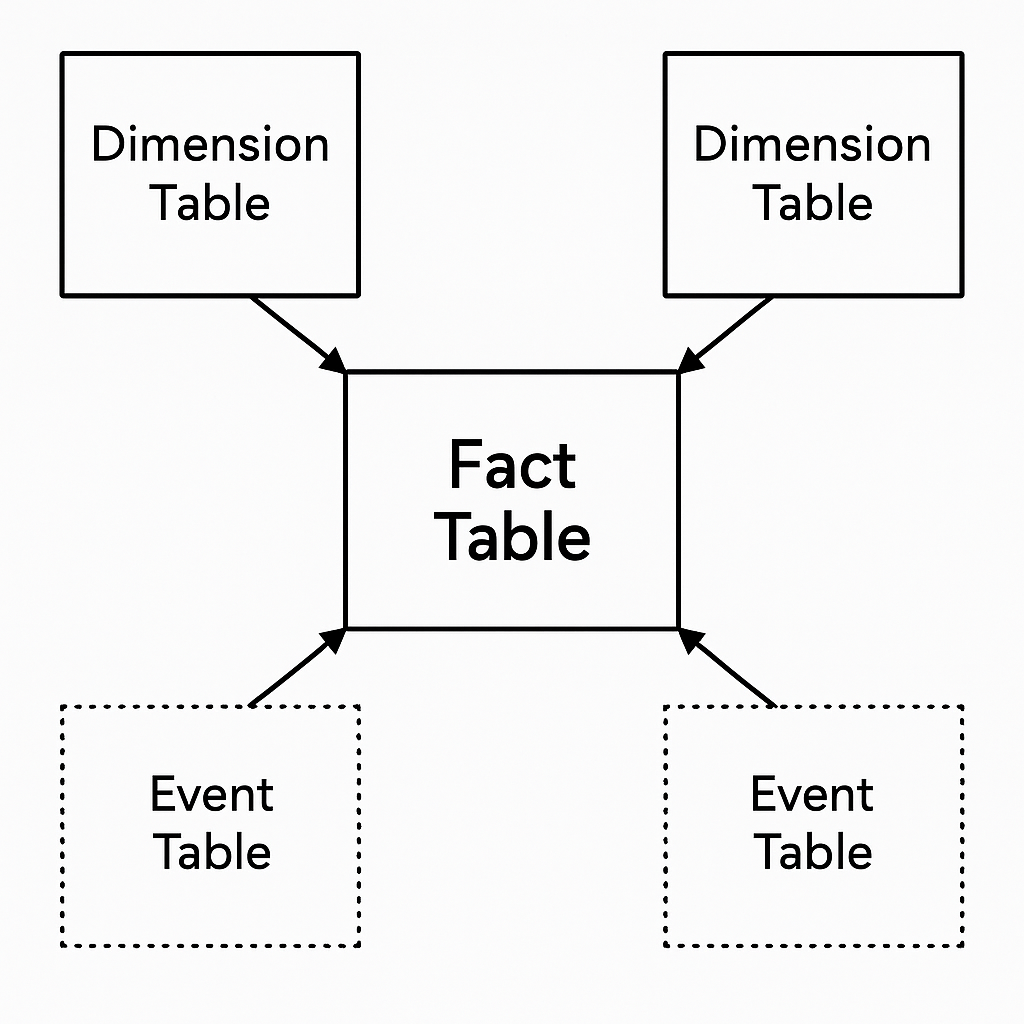

We organize the data using a star schema—a common pattern in financial data warehouses. Since this is not a book about database architecture, we will not dive deep into schema design. However, you need to be aware that financial data warehouses share a common data architecture pattern. The center consists of fact tables (dense, regularly updated data like prices, volumes), surrounded by dimension tables (metadata that changes slowly) and event tables (sparse, irregular occurrences).

Here's what each dataset represents:

dataset

contents (abridged)

role

when you'll use it

prices_daily.csv

tidy OHLCV + ticker identifiers for large-cap stocks/ETFs

Total return calculations, dividend yield features

options.csv

option chain quotes with strikes, expiries, Greeks

event

Volatility surface modeling, hedging strategies

analyst_recommendations.csv

upgrades/downgrades and target changes

event

Sentiment features, recommendation signals

ownership.csv

institutional holders and positions

cross-sectional

Ownership concentration factors

insider_transactions.csv

officer/director trades with roles, amounts, and cash value

event

Insider trading signals, corporate governance features

finance.csv

sample daily finance data from kaggle competition

overall

sample data for this section.

The star schema separates concerns cleanly. Dense fact tables (prices, fundamentals) are optimized for time-series operations. Sparse event tables (dividends, earnings) are joined in only when needed, avoiding memory bloat. Dimension tables (company info) provide stable metadata for cross-sectional analysis.

Why Star Schema for Finance AI:

Separation of Concerns:

Fact tables (prices, fundamentals) = Data that changes over time, optimized for time-series operations

Dimension tables (company info) = Metadata that changes slowly, provides stable reference data

Event tables (dividends, earnings) = Sparse, irregular occurrences that are joined only when needed

Memory Efficiency:

Load only what you need: start with fact tables (prices), join dimensions and events only when required

Example: Load price data first, then join dividend information only for total return calculations

Avoids loading entire event history into memory when you only need recent events

Query Performance:

Fact tables are optimized for time-series operations (rolling, grouping by date)

Dimension tables enable fast lookups for cross-sectional analysis

Event tables can be filtered before joining (e.g., only recent dividends)

Flexibility:

Build different feature sets by joining different combinations of tables

Easy to add new data sources without restructuring existing tables

Practical Example: Building a Feature Set

# Step 1: Load fact table (prices) - your core dataprices = pl.read_csv("data/prices_daily.csv", try_parse_dates=True)# Step 2: Join dimension table (company info) for cross-sectional featurescompany_info = pl.read_csv("data/company_info.csv")prices_with_metadata = prices.join(company_info, on="Ticker", how="left")# Step 3: Join event table (dividends) only when needed for total returnsdividends = ( pl.read_csv("data/corporate_actions.csv", try_parse_dates=True) .filter(pl.col("ActionType") == "dividend") .select(["Date", "Ticker", "Value"]) .rename({"Value": "Dividend"}))# Join events with time-aware join (no look-ahead bias)features = ( prices_with_metadata .join_asof( dividends.sort("Date"), left_on="Date", right_on="Date", by="Ticker", strategy="backward" ) .with_columns(pl.col("Dividend").fill_null(0.0)) .with_columns([ # Total return = price return + dividend yield (pl.col("Return") + pl.col("Dividend") / pl.col("Close")).alias("TotalReturn") ]))

Workflow Pattern:

Start with fact tables (prices) - this is your core time-series data

Join dimensions (company info) - for cross-sectional features and filtering

Join events (dividends, earnings) - for event-driven features, using time-aware joins

Build final feature matrix - combine all information for ML models

After all, in financial AI systems, all we need to know are "What will price be" and "How much to buy". The star schema is the best design for this because it separates the core time-series data (fact tables) from supporting information (dimensions and events). All the edge tables (dimensions, events) are just for providing useful information to build the final dataframe(s) that will inform the system's predictions and decisions.

This pattern appears throughout the book—when building forecasting features (Chapter 4), constructing factors (Chapter 6), and preparing data for AI agents (Chapter 8).

Explanatory Data Analysis with Polars

Let's start with exploring the data using Polars. In finance, it is always important to inspect your data before anything. Not only do data quality issues cause subtle bugs, but you also need to find meaningful patterns with intuition in order to do proper forecasting and dynamic modeling.

Why EDA Matters in Finance:

Data Quality Issues:

Missing prices, incorrect dates, or invalid values can break return calculations

Example: A single bad price can corrupt an entire backtest, leading to incorrect trading signals

Schema validation and sanity checks catch these issues early

Pattern Discovery:

Market regimes: Identify bull/bear markets, volatility regimes, and structural breaks

Volatility clustering: High volatility periods followed by high volatility (GARCH effects)

Cross-asset relationships: Correlations that change over time, factor exposures

AI Limitations and Human Guidance:

One common misconception about artificial intelligence in finance is that AI will solve everything. That's not true.

AI has the capability of processing vast amounts of information, but it is the human's job to guide it to make the right decision.

In fact, because finance and economics mostly face data scarcity issues (limited historical data, regime changes), relying solely on deep learning or AI agents is likely to cause more harm than good.

EDA helps you understand what patterns exist, what assumptions are reasonable, and when models might break

Validation of Assumptions:

Statistical models assume certain distributions (e.g., returns are normally distributed)

EDA reveals when assumptions are violated (fat tails, skewness, non-stationarity)

This informs model choice: use robust methods when assumptions fail

Data Quality Checklist:

Before building models, validate your data:

Schema validation: Expected columns and types match actual data

Price bounds: Prices should be positive and within reasonable ranges

OHLC relationships: High >= Low, High >= max(Open, Close), Low <= min(Open, Close)

Volume: Non-negative, and zero volume should only occur on non-trading days

Returns: Daily returns typically within -50% to +50% (adjust for asset class)

Date ranges: Dates should be within expected historical range

Missing data patterns: Concentrated (one ticker) vs. widespread (all tickers on same dates)

Temporal ordering: No future data leakage (dates should be sorted, no look-ahead)

Connection to Visualization:

EDA is closely tied to visualization (Section 2). Visual inspection helps identify:

Relationships between variables (correlations, scatter plots)

We'll cover visualization patterns in Section 2 that complement the Polars operations shown here.

In terms of polars and csv, a csv file might have dates as strings, volumes as nullable integers, or missing values represented as empty strings. Polars doesn't carry an implicit index like pandas, so every join, filter, or resample must reference explicit columns—making schema validation critical.

finance.csv data

Let's start with simple explanatory analysis with finance.csv data from kaggle competition for daily market prediction portfolio optimization. We start with this data because it is simplest, preprocessed, frequency synchronized data which is easy for us to dive into polars dataframe. You can run head, describe methods to check the basic data structure.

import polars as pldf = pl.read_csv("./data/finance.csv")print(df.head())print(df.describe())

Missing values: Many columns have significant sparsity (e.g., E7: 77% missing, V10: 67% missing)

As you can see from the result, despite the fact that data is already processed, there are lots of NaN values. This is one of the crucial issues in financial data since data frequencies differ and observed times differ. For example:

Different frequencies: Some features might be computed daily, others weekly or monthly

Market holidays: Create gaps in time series (no trading data on weekends/holidays)

Corporate actions: Stock splits, delistings create missing periods

Data source timing: Different data providers update at different times

We will deal with this throughout this book with various strategies:

Forward-fill: For slowly-changing variables (e.g., fundamentals within a quarter)

Zero-fill: For missing returns (assuming no price change)

Drop rows: For extended gaps (e.g., delisted stocks)

Missing indicators: Add features that flag when data is imputed

The key is to handle missing data in a way that doesn't introduce look-ahead bias—a critical concern for backtesting and model validation.

Column and Row Operations

Polars uses an expression-based API that feels like writing SQL queries. Instead of pandas' df.loc indexing, you compose vectorized expressions that operate on entire columns at once. This approach is faster, more readable, and naturally parallelizes across your CPU cores.

Why this matters for finance: Financial workflows involve many column transformations (computing returns, rolling statistics, conditional logic). Polars' expression syntax lets you declare these transformations clearly, and the query optimizer fuses them into efficient pipelines. You write readable code; Polars handles the performance.

Select and Filter

Selecting Columns:

The select() method chooses which columns to keep. You can select by name, use expressions, or combine both:

# Select specific columns by namedf.select(["Date", "Ticker", "Close", "Volume"])# Select with expressions (compute new columns on the fly)df.select([ pl.col("Close"), pl.col("Volume"), (pl.col("Close") * pl.col("Volume")).alias("DollarVolume"), pl.col("Date").dt.year().alias("Year"),])# Select all columns except somedf.select([pl.all().exclude(["UnwantedCol1", "UnwantedCol2"])])

Filtering Rows:

The filter() method keeps rows that match conditions. Use boolean expressions with & (and), | (or), and ~ (not):

Performance Tip: In lazy mode, filters are pushed down to the data source, reducing I/O. Always filter before expensive operations like joins or aggregations.

Computing New Columns

Another important and most commonly used operation is column creation. The with_columns() method is your workhorse for feature engineering. It lets you compute multiple new columns in one pass, keeping related transformations together.

Basic Usage:

# Single columndf = df.with_columns([ (pl.col("Close") * 2).alias("CloseDoubled")])# Multiple columns in one pass (more efficient)df = df.with_columns([ (pl.col("Close") * 2).alias("CloseDoubled"), (pl.col("Close") + pl.col("Open")).alias("ClosePlusOpen"), pl.col("Volume").log().alias("LogVolume"),])

Conditional Logic with pl.when().then().otherwise():

Create columns based on conditions—essential for regime indicators and categorical features:

Single Pass: All columns computed in one operation, reducing memory usage

Query Optimization: Polars can optimize the entire expression pipeline

Readability: Related transformations are grouped together

Performance: Vectorized operations are automatically parallelized

Best Practice: Group related feature engineering steps in a single with_columns() call. This helps Polars optimize the computation and makes your code more maintainable.

Note: Early rows show null values because V1 and V2 columns have missing data at the beginning of the dataset. Later rows (e.g., date_id >= 8000) contain actual values.

Computing Returns and Normalized Features

Returns are the foundation of most financial analysis. You'll also need normalized features (z-scores) for comparing assets with different scales, and lags for momentum and autoregressive models.

Problem: Compute daily returns, normalize them per asset, and create lagged features for forecasting.

per_ticker = prices.sort(["Ticker", "Date"]).with_columns([ # Daily returns (percentage change) ((pl.col("Close") / pl.col("Close").shift(1)) - 1) .over("Ticker") .alias("Return"), # Z-score normalization (standardize returns for cross-asset comparison) ((pl.col("Return") - pl.col("Return").mean().over("Ticker")) / pl.col("Return").std().over("Ticker")) .alias("ReturnZ"), # Lagged return (for momentum and autoregressive features) pl.col("Return").shift(1).over("Ticker").alias("ReturnLag1"),])# Use: Building features for forecasting models, identifying regime changes, # comparing asset performance on normalized scale

Key insight: The .over("Ticker") clause ensures each operation happens within each asset's time series. Without it, you'd mix data across different stocks—a critical bug in panel data.

When to use:

Returns: Essential for any return-based analysis (forecasting, risk, performance)

Z-scores: When comparing assets with different volatility (factor construction, ranking)

Lags: For momentum signals, autoregressive models, and feature engineering

Object-Oriented Operations

In financial data, it is often useful to combine operations into functions or classes. This promotes code reuse, maintainability, and testing—especially important when the same feature engineering pipelines are used across multiple models or backtests.

Function-Based Approach:

Create reusable functions for common feature engineering tasks:

Reusability: Same feature engineering across multiple models, backtests, and experiments

Maintainability: Centralized logic makes updates easier (e.g., changing volatility calculation)

Testing: Easier to unit test feature engineering in isolation

Configuration: Easy to parameterize (windows, thresholds, etc.) without code duplication

Integration: Can combine with visualization (Section 2) and model training (Chapter 4)

Connection to Visualization:

Feature engineering classes can include visualization methods for EDA and model interpretation:

class FeatureEngineer: # ... feature engineering methods ... def plot_feature_distributions(self, df: pl.DataFrame): """Visualize feature distributions (see Section 2).""" # Visualization code here pass

This pattern appears throughout the book—in forecasting models (Chapter 4), where feature engineering classes prepare data for tree-based and neural models.

Multi-Table Joins and Panels

Financial analysis requires combining multiple data sources: prices, fundamentals, events, and metadata. Joins are how you bring these pieces together. But joins in finance come with a critical constraint: you must never use future information (look-ahead bias). This section shows how to join correctly.

Why joins matter: Real financial workflows combine dozens of tables. Prices come from exchanges, fundamentals from company filings, events from news feeds, and metadata from reference data providers. Joins let you build rich feature sets while maintaining data integrity.

Point-in-Time Snapshots

Business question: "What are the latest prices and returns for each stock, along with their company metadata?"

This pattern creates a cross-sectional snapshot—useful for portfolio construction, ranking, and initializing models with current market state.

info = pl.read_csv("data/company_info.csv")pt_snapshot = ( prices.sort(["Ticker", "Date"]) .group_by("Ticker") .tail(1) # latest row per ticker .select(["Ticker", "Date", "Close", "Return"]) .join(info, on="Ticker", how="left"))# Use: Cross-sectional ranking (rank stocks by current metrics),# Portfolio initialization (select holdings based on latest data),# Model feature preparation (combine price and fundamental features)

When to use: Cross-sectional analysis, portfolio construction, and any workflow that needs "current state" of all assets.

Join type choice: how="left" keeps all price records even if metadata is missing. Use how="inner" if you only want stocks with complete metadata.

Joining Sparse Events to Dense Prices

Business question: "For each trading day, what dividends were paid, and how do they affect total returns?"

Events (dividends, earnings, splits) occur sporadically but must align precisely with price data. This join pattern handles sparse events correctly.

actions = ( pl.read_csv("data/corporate_actions.csv", try_parse_dates=True) .with_columns(pl.col("Date").cast(pl.Date)))dividends = ( actions.filter(pl.col("ActionType") == "dividend") .select(["Date", "Ticker", "Value"]) .rename({"Value": "Dividend"}))prices_with_div = ( prices.join(dividends, on=["Ticker", "Date"], how="left") .with_columns(pl.col("Dividend").fill_null(0.0)))# Use: Computing total returns (price return + dividend yield),# Building dividend yield features for forecasting,# Adjusting prices for corporate actions

Critical warning—avoiding look-ahead bias: This join uses exact date matching (on=["Ticker", "Date"]), which is correct for dividends that are known on the ex-date. However, if you're joining earnings announcements or other forward-looking events, you must use join_asof with strategy="backward" to ensure you only use information available at that point in time. See the "Event Joins Without Look-Ahead" pattern below.

When to use: Any sparse event that occurs on specific dates (dividends, splits, earnings announcements) that you need to align with daily price data.

Panel Reshaping: Long vs. Wide Format

Business question: "I need to feed price data into a neural network that expects a wide matrix format, then convert back to long format for analysis."

Financial data is typically stored in "long" format (one row per asset-date combination), but some operations (matrix operations, correlation calculations) require "wide" format (one column per asset). Polars lets you convert between formats efficiently.

# Convert long to wide (one column per ticker)panel_long = prices.select(["Date", "Ticker", "Close"])panel_wide = panel_long.pivot(values="Close", index="Date", on="Ticker")# Convert wide back to long (restore tidy format)panel_long_again = panel_wide.melt( id_vars="Date", variable_name="Ticker", value_name="Close",)# Use: Feeding wide matrices into NumPy/PyTorch layers for cross-asset models,# Computing correlation matrices across assets,# Then reverting to long format for per-asset analysis

Memory trade-off: Wide matrices are convenient for matrix operations but consume more memory (one column per asset). For large universes (thousands of assets), prefer long format with lazy evaluation to keep memory bounded.

Note: melt is being replaced by unpivot in newer Polars releases. Use unpivot if your version supports it.

When to Use Each Join Type

how="left": Keep all rows from the left table (prices), add matching data from right. Use when you want to preserve all price records even if events are missing.

how="inner": Keep only rows that match in both tables. Use when you need complete data and missing values would break your analysis.

how="asof": Match on nearest key (typically date) with direction. Use for aligning events that don't occur on exact trading dates (earnings announced after market close, but you want to associate them with the next trading day).

Look-ahead bias warning: Always ensure your joins only use information available at that point in time. For forward-looking events (earnings, analyst upgrades), use join_asof with strategy="backward" and a tolerance window to ensure you're not peeking into the future.

Missing Data and Large Pipelines

Financial data is messy. Prices have gaps (holidays, delistings), fundamentals arrive late (earnings reported weeks after quarter-end), and arithmetic operations produce NaNs (division by zero, log of negative values). How you handle missing data determines whether your models are realistic or biased.

The two types of missingness:

marker

meaning

example in finance

null

source missingness (no record exists)

Holiday with no trading data, delisted stock

NaN

arithmetic artifact (computation produced invalid result)

Log of negative price, division by zero in return calculation

Why this distinction matters: null represents genuine data gaps (you can't trade on holidays). NaN represents computational errors (your formula broke). They require different handling strategies.

Inspecting Missing Data

First, understand the pattern of missingness:

# Count missing values per columnmissing = prices.select([ pl.col("Return").is_null().sum().alias("Nulls"), pl.col("Return").is_not_null().sum().alias("NonNulls"),])# Check which tickers have the most gapsmissing_by_ticker = ( prices.group_by("Ticker") .agg(pl.col("Return").is_null().sum().alias("MissingDays")) .sort("MissingDays", descending=True))

What to look for: Concentrated missingness (one ticker has many gaps) suggests data quality issues. Widespread missingness (all tickers missing on same dates) suggests calendar effects (holidays, market closures).

This shows that many columns have significant missing data, with E7 having 77% missing values (6,969 out of 9,021 rows). This is typical in financial datasets where different features are computed at different frequencies or become available at different times.

Handling Missing Data: Decision Guide

The right strategy depends on your use case. Here's a decision framework:

Strategy 1: Drop Missing Rows

When to use: Backtesting, where you need complete data and can tolerate excluding incomplete periods.

# Drop rows with missing returns or volumesclean_backtest = prices.drop_nulls(["Return", "Volume"])

Pros: Simple, preserves data integrity, no imputation assumptions.

Cons: Reduces sample size, may introduce survivorship bias if you drop delisted stocks.

Critical warning: Never drop rows based on future data. If you're backtesting, only drop based on data available at that point in time.

Strategy 2: Fill with Zero or Constant

When to use: Forecast feature engineering, where models expect dense tensors and zeros represent "no signal."

# Fill missing returns with zero (assumes no price change)forecast_fill = prices.with_columns(pl.col("Return").fill_null(0.0))

Pros: Preserves sample size, works with models that can't handle missing values.

Cons: Assumes missing = zero, which may not be realistic. Document this assumption clearly.

When appropriate: Short-term gaps (single days) where zero return is a reasonable assumption. Not appropriate for extended gaps (delistings, where zero return is misleading).

Example with finance.csv:

# Fill missing with zerofilled = df.select(["V1", "V2", "V3"]).with_columns([ pl.col("V1").cast(pl.Float64, strict=False).fill_null(0.0).alias("V1_filled"), pl.col("V2").cast(pl.Float64, strict=False).fill_null(0.0).alias("V2_filled")])print(filled.head())

Strategy 3: Forward Fill (Carry Last Value Forward)

When to use: Fundamentals and metadata that change slowly, where the last known value is a reasonable proxy.

# Forward-fill returns within each ticker (carry last return forward)factor_ffill = ( prices.sort(["Ticker", "Date"]) .with_columns( pl.col("Return").fill_null(strategy="forward") .over("Ticker") .alias("Return_ffill") ))

Pros: Preserves sample size, reasonable for slowly-changing variables.

Cons: Creates look-ahead bias if used incorrectly. Only forward-fill within known windows (e.g., within a quarter for fundamentals). Never forward-fill across major events (earnings, delistings).

Critical warning for backtesting: Forward-filling future data is look-ahead bias. If you're backtesting and forward-fill, ensure you only use data available at that point in time. For example, if earnings are reported on day T, don't forward-fill earnings data before day T—that's using future information.

Use-Case Specific Guidance

Backtests: Tolerate row drops (drop_nulls) but never forward-fill future data. Always validate that your missing data handling doesn't introduce look-ahead bias.

Forecast features: Can fill NaNs with zeros if the model expects dense tensors, but document the imputation clearly. Consider using a separate "missing" indicator feature to let the model learn that zeros might be imputed.

Fundamentals: Should only be forward-filled within report windows (e.g., quarterly earnings are known for the entire quarter). Never forward-fill across reporting boundaries—that's look-ahead bias.

Price data: For short gaps (holidays), forward-fill is reasonable. For extended gaps (delistings), drop the rows or mark them explicitly.

Best practice: Always add a "was_missing" indicator column when you impute. This lets downstream models distinguish real zeros from imputed zeros, improving model quality.

Lazy Execution: Building Efficient Pipelines

Most production pipelines should stay in lazy mode until the very end. Lazy execution lets Polars optimize your entire query before running it, often delivering 10-100x speedups on large datasets. Think of it as giving Polars a "blueprint" of your entire pipeline so it can optimize the execution plan.

When lazy execution matters:

Large datasets (millions of rows, thousands of assets)

Production pipelines that run daily/hourly

Feature engineering workflows with many transformations

Any workflow where performance matters

When you can skip it: Small datasets (<100K rows), one-off analyses, or when you need immediate results for debugging.

The Lazy Execution Pattern

Here's a complete template showing a typical finance workflow in lazy mode:

What happens under the hood: Polars builds a query plan, optimizes it (predicate pushdown, projection pruning, operator fusion), then executes it efficiently. The .collect() call triggers actual execution.

Why Lazy Execution is Faster

1. Predicate pushdown: Filters run before reading data from disk.

Example: If you filter Volume > 0 early, Polars can skip reading rows that will be filtered out, reducing I/O.

Finance impact: When processing years of daily data for thousands of assets, filtering early (e.g., removing delisted stocks, focusing on liquid assets) dramatically reduces memory usage and I/O time.

2. Projection pruning: Unused columns are never materialized.

Example: If you only need Date, Ticker, and Close, Polars won't load Open, High, Low, Volume from disk.

Finance impact: Price files often have many columns (OHLCV, adjusted prices, volumes). Selecting only what you need can cut memory usage by 50-80%.

3. Operator fusion: Chained expressions become single optimized kernels.

Example: (Close / Close.shift(1) - 1).over("Ticker") fuses into one operation instead of three separate passes.

Finance impact: Feature engineering often involves many chained operations. Fusion reduces intermediate memory allocations and improves cache locality.

4. Parallel scheduling: Polars spreads independent operations across CPU cores.

Example: Computing rolling statistics for different tickers can run in parallel.

Finance impact: With thousands of assets, parallelization provides near-linear speedup on multi-core machines.

Before/After: Lazy vs. Eager Execution

Eager execution (materializes at each step):

# Each step materializes data, using more memory and timeprices_eager = pl.read_csv("data/prices_daily.csv")prices_filtered = prices_eager.filter(pl.col("Volume") > 0) # Materializedprices_with_returns = prices_filtered.with_columns([...]) # Materialized againmonthly = prices_with_returns.group_by_dynamic(...) # Materialized again

Lazy execution (optimizes entire pipeline):

# Single optimized execution planresult = ( pl.scan_csv("data/prices_daily.csv") # Lazy from the start .filter(pl.col("Volume") > 0) .with_columns([...]) .group_by_dynamic(...) .collect() # Materialize only once, at the end)

Performance difference: On a 10GB dataset with 1000 assets over 10 years, lazy execution typically runs 5-10x faster and uses 50-70% less memory.

Essential Patterns Cheat Sheet

Cast dates explicitly: Never operate on string timestamps. Cast to Date type immediately after reading.

Keep transformations in with_columns: Polars can optimize expressions inside with_columns better than separate operations.

Use .over("Ticker") for per-asset operations: Any lag, rank, or normalization that should happen within each asset group needs .over("Ticker").

Use group_by_dynamic for calendar time: When you mean calendar months/quarters/weeks, not fixed row counts, use group_by_dynamic instead of fixed windows.

Document missing data handling: Missing data is part of financial reality. Document when you drop, fill, or forward-carry, and why.

Stay lazy until the end: Keep pipelines lazy until you truly need materialized output (e.g., converting to NumPy for PyTorch, writing to disk, or displaying results).

Profile representative data: Run lazy().explain() to see the query plan. Profile on a sample (10-20% of data) to validate performance before running on full dataset.

Filter early, select late: Apply filters as early as possible (reduces data size). Select columns only when you know what you need (but before expensive operations).

Use streaming for very large datasets: For datasets that don't fit in memory, add streaming=True to scan_csv or scan_parquet. Polars will process in chunks.

Avoid converting to pandas: Converting to pandas breaks lazy evaluation and forces materialization. Only convert when absolutely necessary (e.g., for libraries that require pandas).

Columnar Patterns for Financial Panels

This section covers advanced patterns that appear frequently in production finance systems. These patterns combine multiple Polars operations to solve complex financial data problems.

Rolling Features with Grouped Context

Problem: Build alpha factors that require rolling statistics computed independently for each asset.

Windowed statistics (moving averages, rolling volatility, autocorrelations) are the building blocks of many quantitative strategies. Polars window functions compute these per group without manual loops, making them fast and readable.

Use case: Factor construction, where you compute rolling momentum, volatility, and mean-reversion signals for each asset independently.

# Compute returns firstreturns = prices.lazy().sort(["Ticker", "Date"]).with_columns( pl.col("AdjClose").pct_change().over("Ticker").alias("ret"), pl.col("AdjClose").log().diff().over("Ticker").alias("log_ret"),)# Build rolling features per tickerfeatures = returns.with_columns( # 21-day rolling mean return (momentum signal) pl.col("log_ret").rolling_mean(window_size=21).over("Ticker").alias("ret_1m"), # 21-day rolling volatility (risk measure) pl.col("log_ret").rolling_std(window_size=21).over("Ticker").alias("vol_1m"), # First-order autocorrelation (mean-reversion signal) pl.corr("log_ret", pl.col("log_ret").shift(1), ddof=0) .over("Ticker") .alias("auto1"),)

Why this pattern matters: Many quantitative strategies rely on rolling features (momentum, volatility, mean-reversion). Computing them efficiently across thousands of assets requires vectorized operations. Polars' window functions handle this automatically.

Performance tip: Keep operations in lazy mode and use .over("Ticker") to ensure computations happen per asset. This enables parallelization across assets.

Event Joins Without Look-Ahead Bias

Problem: Align sparse events (earnings, dividends, corporate actions) with price data without using future information.

Events don't always occur on exact trading dates. Earnings might be announced after market close, but you want to associate them with the next trading day. join_asof handles this correctly, ensuring you only use information available at that point in time.

Use case: Building event-driven features (earnings surprise, dividend yield) for forecasting models, ensuring no look-ahead bias.

events = pl.read_csv("data/corporate_actions.csv", try_parse_dates=True)joined = ( prices.lazy() .join_asof( events.lazy(), left_on="Date", # Trading dates right_on="ExDate", # Event dates by="Ticker", # Match within each asset strategy="backward", # Use most recent event before/on this date tolerance=pl.duration(days=3), # Only match events within 3 days ) .with_columns(pl.col("Dividend").fill_null(0)))

Why strategy="backward" matters: This ensures you only use events that occurred on or before the trading date. Using strategy="forward" would be look-ahead bias—using future information in your model.

When to use: Any event that doesn't align perfectly with trading dates: earnings announcements, analyst upgrades, corporate actions. The tolerance window handles cases where events occur on weekends or holidays.

Multi-Market Calendars and Resampling

Problem: Assets trade on different calendars (NYSE vs. NASDAQ holidays, international markets with different time zones). You need to aggregate them to a common frequency.

Solution: Build a master calendar (all trading days across all exchanges), then join each asset's data to it with forward-fill. Use group_by_dynamic to resample to common frequencies (daily, weekly, monthly) while respecting calendar boundaries.

Use case: Cross-asset factor models, where you need all assets aligned to the same calendar for correlation and covariance calculations.

Join each asset with forward-fill: asset.join(master_cal, on="Date", how="outer").sort("Date").with_columns(pl.col("Close").forward_fill())

Resample to target frequency: group_by_dynamic("Date", every="1w")

Why this matters: Different exchanges have different holidays. Without alignment, you can't compute cross-asset correlations or build factor models that require synchronized data.

Streaming and Out-of-Core Processing

Problem: Intraday data (tick-by-tick trades) doesn't fit in memory. You need to process it in chunks.

Solution: Use Polars' streaming mode to process data in batches, keeping memory bounded.

Use case: Processing intraday trade data, building minute/hourly bars from tick data, or processing large historical datasets that exceed available RAM.

# Process large intraday dataset in streaming modelarge = pl.scan_parquet("s3://bucket/trades/*.parquet", streaming=True)# Aggregate to 5-minute barsbinned = large.group_by_dynamic("ts", every="5m", by="Ticker").agg( pl.col("price").mean().alias("vwap"), # Volume-weighted average price pl.col("size").sum().alias("volume"), # Total volume)

When to use streaming:

Datasets larger than available RAM

Incremental processing (update features daily without reprocessing entire history)

MLOps pipelines that process new data as it arrives

Performance tip: Streaming mode processes data in chunks, so it's slightly slower than in-memory processing but enables handling datasets of any size. Use it when memory is the constraint, not compute.

Finance-specific note: Intraday data can be terabytes in size. Streaming mode lets you build features and aggregate to daily frequency without loading everything into memory, making it essential for production systems processing high-frequency data.

Common Finance Workflows

This section shows complete end-to-end workflows that combine multiple Polars patterns. These are the kinds of pipelines you'll build in production systems.

Workflow 1: Building Features for a Forecasting Model

Goal: Prepare a feature matrix for training a return forecasting model. Features include returns, rolling statistics, and calendar features.

Steps:

Load and inspect price data

Compute returns and rolling statistics

Add calendar features

Handle missing data

Export to NumPy for model training

import polars as plimport numpy as np# Step 1: Load and inspectprices = ( pl.read_csv("data/prices_daily.csv", try_parse_dates=True) .with_columns(pl.col("Date").cast(pl.Date)) .sort(["Ticker", "Date"]))# Step 2: Compute returns and rolling featuresfeatures = prices.lazy().with_columns([ # Returns ((pl.col("Close") / pl.col("Close").shift(1)) - 1) .over("Ticker") .alias("Return"), # Rolling statistics (21-day window) pl.col("Close").rolling_mean(21).over("Ticker").alias("MA21"), pl.col("Close").rolling_std(21).over("Ticker").alias("Vol21"), # Momentum (return over last 5 days) ((pl.col("Close") / pl.col("Close").shift(5)) - 1) .over("Ticker") .alias("Momentum5"),]).with_columns([ # Calendar features pl.col("Date").dt.weekday().alias("Weekday"), pl.col("Date").dt.month().alias("Month"),]).drop_nulls(["Return", "MA21", "Vol21"]).collect()# Step 3: Prepare for model (convert to wide format if needed, or keep long)# For scikit-learn / XGBoost, you might want long format with Ticker as a feature# For neural networks, you might reshape to wide format# Export to NumPyX = features.select(["MA21", "Vol21", "Momentum5", "Weekday", "Month"]).to_numpy()y = features.select("Return").to_numpy()

Key patterns used: Per-ticker operations (.over("Ticker")), rolling windows, calendar features, missing data handling.

Workflow 2: Preparing Data for Backtesting

Goal: Prepare a clean dataset for backtesting a trading strategy, ensuring no look-ahead bias.

Steps:

Load prices and filter for liquid assets

Compute returns and signals

Join with corporate actions (dividends) for total returns

Ensure temporal ordering (no future data leakage)

Export to backtesting framework

# Step 1: Load prices and filterprices = ( pl.read_csv("data/prices_daily.csv", try_parse_dates=True) .with_columns(pl.col("Date").cast(pl.Date)) .filter(pl.col("Volume") > 1_000_000) # Liquidity filter .sort(["Ticker", "Date"]))# Step 2: Compute returns and signalssignals = prices.lazy().with_columns([ ((pl.col("Close") / pl.col("Close").shift(1)) - 1) .over("Ticker") .alias("Return"), # Simple momentum signal ((pl.col("Close") / pl.col("Close").shift(20)) - 1) .over("Ticker") .alias("Momentum20"), # Volatility signal pl.col("Close").rolling_std(20).over("Ticker").alias("Vol20"),]).collect()# Step 3: Join dividends for total returnsdividends = ( pl.read_csv("data/corporate_actions.csv", try_parse_dates=True) .with_columns(pl.col("Date").cast(pl.Date)) .filter(pl.col("ActionType") == "dividend") .select(["Date", "Ticker", "Value"]) .rename({"Value": "Dividend"}))backtest_data = ( signals.lazy() .join(dividends.lazy(), on=["Ticker", "Date"], how="left") .with_columns([ pl.col("Dividend").fill_null(0.0), (pl.col("Return") + pl.col("Dividend") / pl.col("Close")) .alias("TotalReturn"), ]) .drop_nulls(["Return", "Momentum20", "Vol20"]) .collect())# Step 4: Validate temporal ordering (no future data)# This is critical - ensure signals only use past dataassert backtest_data.sort(["Ticker", "Date"]).is_sorted("Date", by="Ticker")

Key patterns used: Filtering, joins, missing data handling, temporal validation.

Workflow 3: Computing Cross-Sectional Factors

Goal: Compute factor values (e.g., value, momentum, quality) for all assets at each point in time, for use in factor models.

Steps:

Load prices and fundamentals

Compute per-asset time-series features

Reshape to wide format for cross-sectional operations

Compute factor scores (rankings, z-scores)

Reshape back to long format

# Step 1: Load dataprices = ( pl.read_csv("data/prices_daily.csv", try_parse_dates=True) .with_columns(pl.col("Date").cast(pl.Date)) .sort(["Ticker", "Date"]))fundamentals = ( pl.read_csv("data/fundamentals.csv", try_parse_dates=True) .with_columns(pl.col("Date").cast(pl.Date)))# Step 2: Compute per-asset featuresasset_features = prices.lazy().with_columns([ ((pl.col("Close") / pl.col("Close").shift(1)) - 1) .over("Ticker") .alias("Return"), # 12-month momentum ((pl.col("Close") / pl.col("Close").shift(252)) - 1) .over("Ticker") .alias("Momentum12M"), # 20-day volatility pl.col("Close").rolling_std(20).over("Ticker").alias("Vol20"),]).collect()# Step 3: Join fundamentals and compute value factor (P/E, P/B, etc.)# This is simplified - real value factors use multiple fundamental ratiosvalue_data = ( asset_features.lazy() .join(fundamentals.lazy(), on=["Ticker", "Date"], how="left") .with_columns([ (pl.col("Close") / pl.col("Earnings")).alias("PE_Ratio"), ]) .collect())# Step 4: Reshape to wide for cross-sectional ranking# For each date, rank all assets by momentum and valuefactors = ( value_data.lazy() .select(["Date", "Ticker", "Momentum12M", "PE_Ratio", "Vol20"]) .with_columns([ # Cross-sectional z-scores (normalize across assets on each date) pl.col("Momentum12M").mean().over("Date").alias("MomMean"), pl.col("Momentum12M").std().over("Date").alias("MomStd"), ]) .with_columns([ ((pl.col("Momentum12M") - pl.col("MomMean")) / pl.col("MomStd")) .alias("MomentumFactor"), # Inverse PE (value factor - lower PE is better) (-pl.col("PE_Ratio")).rank().over("Date").alias("ValueFactorRank"), ]) .select(["Date", "Ticker", "MomentumFactor", "ValueFactorRank", "Vol20"]) .collect())

When to use: Factor construction for multi-factor models, cross-sectional ranking strategies, and risk model construction.

These workflows demonstrate how Polars patterns combine to solve real financial data problems. Each workflow uses multiple patterns from earlier sections, showing how they work together in practice.

Data Quality, Testing, and Contracts

Data quality is critical in finance. A single bad price can break return calculations, corrupt backtests, and lead to incorrect trading decisions. This section shows how to validate your data systematically.

Why data quality matters: Financial models are only as good as their inputs. Missing prices, incorrect dates, or invalid values propagate through your entire pipeline, causing subtle bugs that are expensive to fix. Automated validation catches these issues early.

Schema Contracts

Define expected structure (columns, types, nullability) and validate after every data load. This catches schema drift when data sources change.

import polars as plfrom typing import Dict# Define expected schemaEXPECTED_SCHEMA = { "Date": pl.Date, "Ticker": pl.Utf8, "Open": pl.Float64, "High": pl.Float64, "Low": pl.Float64, "Close": pl.Float64, "Volume": pl.Int64,}def validate_schema(df: pl.DataFrame, expected: Dict[str, pl.DataType]) -> bool: """Validate that DataFrame matches expected schema.""" actual_schema = df.schema for col, expected_type in expected.items(): if col not in actual_schema: raise ValueError(f"Missing column: {col}") if actual_schema[col] != expected_type: raise ValueError( f"Column {col} has type {actual_schema[col]}, expected {expected_type}" ) return True# Use after loading dataprices = pl.read_csv("data/prices_daily.csv", try_parse_dates=True)validate_schema(prices, EXPECTED_SCHEMA)

When to use: After every data load, especially when data comes from external sources (APIs, vendors, file drops). Schema validation catches breaking changes immediately.

Finance-Specific Sanity Checks

Financial data has domain-specific constraints. Validate these to catch data quality issues:

def validate_price_data(df: pl.DataFrame) -> pl.DataFrame: """Run finance-specific validation checks.""" issues = [] # Check 1: Prices should be positive negative_prices = df.filter( (pl.col("Close") <= 0) | (pl.col("Open") <= 0) | (pl.col("High") <= 0) | (pl.col("Low") <= 0) ) if len(negative_prices) > 0: issues.append(f"Found {len(negative_prices)} rows with non-positive prices") # Check 2: High >= Low, High >= Open, High >= Close, Low <= Open, Low <= Close invalid_ohlc = df.filter( (pl.col("High") < pl.col("Low")) | (pl.col("High") < pl.col("Open")) | (pl.col("High") < pl.col("Close")) | (pl.col("Low") > pl.col("Open")) | (pl.col("Low") > pl.col("Close")) ) if len(invalid_ohlc) > 0: issues.append(f"Found {len(invalid_ohlc)} rows with invalid OHLC relationships") # Check 3: Volume should be non-negative negative_volume = df.filter(pl.col("Volume") < 0) if len(negative_volume) > 0: issues.append(f"Found {len(negative_volume)} rows with negative volume") # Check 4: Returns should be within reasonable bounds (e.g., -50% to +50% daily) returns = df.with_columns([ ((pl.col("Close") / pl.col("Close").shift(1)) - 1).over("Ticker").alias("Return") ]) extreme_returns = returns.filter(pl.col("Return").abs() > 0.5) if len(extreme_returns) > 0: issues.append(f"Found {len(extreme_returns)} rows with extreme returns (>50%)") # Check 5: Dates should be in reasonable range (e.g., 2000-2030) invalid_dates = df.filter( (pl.col("Date") < pl.date(2000, 1, 1)) | (pl.col("Date") > pl.date(2030, 12, 31)) ) if len(invalid_dates) > 0: issues.append(f"Found {len(invalid_dates)} rows with dates outside expected range") if issues: raise ValueError("Data quality issues found:\n" + "\n".join(issues)) return df# Use in your pipelineprices = pl.read_csv("data/prices_daily.csv", try_parse_dates=True)prices = validate_price_data(prices)

Common finance checks:

Price bounds: Prices should be positive and within reasonable ranges

OHLC relationships: High >= Low, High >= max(Open, Close), Low <= min(Open, Close)

Volume: Non-negative, and zero volume should only occur on non-trading days

Returns: Daily returns typically within -50% to +50% (adjust for asset class)

Date ranges: Dates should be within expected historical range

Ticker format: Tickers should match expected format (e.g., uppercase, no special characters)

Reconciliation Checks

Cross-verify your computed values against known benchmarks to catch calculation errors.

When to use: After computing critical values (returns, volatilities, factors). Compare against vendor data, published indexes, or known benchmarks to catch calculation bugs.

Embedding Checks in CI/CD

Automate validation in your CI pipeline to catch data quality issues before they reach production:

# In your CI/CD pipeline or data loading scriptdef load_and_validate_prices(filepath: str) -> pl.DataFrame: """Load prices with full validation.""" df = pl.read_csv(filepath, try_parse_dates=True) validate_schema(df, EXPECTED_SCHEMA) df = validate_price_data(df) # Additional checks as needed return df

Best practices:

Run validation after every data load

Fail fast: raise errors immediately when validation fails

Log validation results for monitoring

Version your schema contracts alongside your code

Test with known bad data to ensure validation catches issues

Why this matters for production: Silent data drift (schema changes, new data sources, vendor updates) can break production systems. Automated validation catches these issues before they cause problems.

Performance Optimization

Polars is fast by default, but understanding how to optimize your pipelines helps you handle larger datasets and reduce costs. This section covers practical performance tips for finance workloads.

Inspecting Query Plans

Before optimizing, understand what Polars is doing. Use lazy().explain() to see the optimized query plan:

# See the optimized query planplan = ( prices.lazy() .filter(pl.col("Volume") > 0) .with_columns([...]) .group_by_dynamic("Date", every="1mo") .agg([...]))print(plan.explain())

What to look for:

Predicate pushdown: Filters should appear early in the plan (they reduce data size)

Projection pruning: Only needed columns should be scanned

Operator fusion: Multiple operations should be fused into single kernels

When to use: When a query is slower than expected, or when you want to verify Polars is optimizing correctly.

Finance-Specific Performance Tips

1. Filter early, select late

Apply filters as early as possible to reduce data size. Select columns only when you know what you need, but before expensive operations.

# Good: Filter earlyresult = ( prices.lazy() .filter(pl.col("Volume") > 1_000_000) # Reduce data size early .filter(pl.col("Date") >= pl.date(2020, 1, 1)) .with_columns([...]) # Expensive operations on smaller dataset .select(["Ticker", "Date", "Return"]) # Select only needed columns .collect())# Bad: Filter lateresult = ( prices.lazy() .with_columns([...]) # Expensive operations on full dataset .filter(pl.col("Volume") > 1_000_000) # Filter after expensive work .collect())

2. Use lazy evaluation for large datasets

Keep pipelines lazy until you need materialized output. This enables query optimization and reduces memory usage.

# Good: Lazy until the endresult = prices.lazy().with_columns([...]).group_by([...]).collect()# Bad: Materializing intermediate resultsintermediate = prices.with_columns([...]) # Materializedresult = intermediate.group_by([...]) # Works on materialized data

3. Avoid converting to pandas

Converting to pandas breaks lazy evaluation and forces materialization. Only convert when absolutely necessary (e.g., for libraries that require pandas).

For datasets that don't fit in memory, enable streaming mode:

# Enable streaming for large fileslarge = pl.scan_parquet("s3://bucket/data/*.parquet", streaming=True)result = large.group_by([...]).agg([...]).collect()

When to use: Datasets larger than available RAM, or when processing incremental updates.

5. Profile on representative samples

Before running on full datasets, profile on a sample (10-20%) to validate performance:

# Profile on samplesample = prices.filter(pl.col("Date") >= pl.date(2023, 1, 1)) # Recent 20% of data# Run your pipeline on sample and measure time# Then scale up to full dataset

Pitfall 2: Using apply for vectorizable operations

# Bad: apply is slowresult = df.with_columns([ pl.col("Return").apply(lambda x: x * 2).alias("DoubleReturn")])# Good: Use built-in expressionsresult = df.with_columns([ (pl.col("Return") * 2).alias("DoubleReturn")])

Pitfall 3: Not using .over() for grouped operations

# Bad: Computes mean across all data, then filtersresult = df.with_columns([ (pl.col("Return") - pl.col("Return").mean()).alias("Deviation")]).filter(pl.col("Ticker") == "AAPL")# Good: Compute mean per groupresult = df.with_columns([ (pl.col("Return") - pl.col("Return").mean().over("Ticker")).alias("Deviation")])

When I/O Dominates

If reading data is the bottleneck (large files, slow network, many small files):

Compress data: Use Parquet with compression (Zstandard or Snappy)

Column pruning: Select only needed columns before reading

Predicate pushdown: Filter early so Polars can skip reading irrelevant rows

Batch processing: Process files in batches rather than loading everything

# Example: Efficient I/O with column pruning and filteringresult = ( pl.scan_parquet("data/*.parquet") .select(["Ticker", "Date", "Close"]) # Only read needed columns .filter(pl.col("Date") >= pl.date(2020, 1, 1)) # Filter early .collect())

When Compute Dominates

If computation is the bottleneck (many transformations, complex aggregations):

Use built-in expressions: Avoid apply for operations that can be vectorized

Operator fusion: Keep related operations together so Polars can fuse them

Parallelization: Polars automatically parallelizes across cores; ensure operations are parallelizable (avoid Python UDFs)

Profile and optimize: Use explain() to see if operations are being fused

# Good: Operations that can be fusedresult = df.with_columns([ pl.col("Return") * 2, pl.col("Return") + 1, pl.col("Return").abs(),]) # These can be fused into one pass# Bad: Operations that can't be fused easilyresult = df.with_columns([ pl.col("Return").apply(lambda x: complex_function(x))]) # Python UDF prevents fusion

Monitoring Performance

Key metrics to track:

Execution time: How long queries take

Memory usage: Peak memory consumption

I/O time: Time spent reading/writing data

CPU utilization: Whether you're using all available cores

Tools:

lazy().explain(): See query plan

Python's timeit or cProfile: Measure execution time

System monitoring tools: Track memory and CPU usage

Best practice: Profile once on representative data to establish baselines, then monitor for regressions as your data grows or code changes.

Financial Data Visualization

After processing financial data with Polars (Section 1), visualization helps us understand patterns, validate assumptions, and communicate results. This section covers practical visualization patterns for exploratory data analysis (EDA), model interpretation, and publication-ready figures.

Why Visualization Matters for Financial AI

Visualization serves multiple critical roles in financial AI workflows:

Exploratory Data Analysis (EDA): Discover data quality issues, identify market regimes, validate statistical assumptions, and find patterns that inform feature engineering

Model Interpretation: Understand model predictions, debug failures, identify when models break, and communicate results to stakeholders

Validation: Verify that data processing is correct (e.g., returns are computed properly, joins align correctly), and check that models behave as expected

Communication: Present findings, backtest results, and model performance to teams, clients, or in research publications

Connection to Other Chapters: Visualization patterns introduced here are used throughout the book—for forecasting results (Chapter 4), factor analysis (Chapter 6), and model diagnostics.

Polars to Visualization: Converting DataFrames

Polars DataFrames need to be converted for most visualization libraries (matplotlib, seaborn, plotly), which expect pandas DataFrames or NumPy arrays. Here's how to do it efficiently.

Converting to Pandas

Most visualization libraries work with pandas, so convert Polars DataFrames when needed:

import polars as plimport matplotlib.pyplot as pltimport seaborn as sns# Load and process data with Polarsprices = ( pl.scan_csv("data/prices_daily.csv", try_parse_dates=True) .filter(pl.col("Ticker") == "AAPL") .sort("Date") .with_columns([ ((pl.col("Close") / pl.col("Close").shift(1)) - 1).alias("Return") ]))# Convert to pandas for visualization (only materialize what you need)prices_pd = prices.select(["Date", "Close", "Return"]).collect().to_pandas()prices_pd.set_index("Date", inplace=True)# Now use with matplotlib/seabornplt.figure(figsize=(12, 6))plt.plot(prices_pd.index, prices_pd["Close"])plt.title("AAPL Price Series")plt.show()

Example with finance.csv:

# Load data with Polarsdf = pl.read_csv("data/finance.csv")# Convert to pandas (select only needed columns)df_viz = df.select(["date_id", "forward_returns", "risk_free_rate", "market_forward_excess_returns"])df_pd = df_viz.to_pandas()print(df_pd.head())

Best Practice: Keep data in Polars for processing, convert to pandas/NumPy only at the visualization boundary. This maintains lazy evaluation benefits and reduces memory usage.

EDA Visualization Patterns

Exploratory data analysis visualization helps you understand your data before modeling. These patterns are essential for identifying issues and discovering patterns.

Distribution Plots

Understanding the distribution of returns, volatility, and features is fundamental.

Returns Distribution:

import polars as plimport matplotlib.pyplot as pltimport seaborn as snsimport numpy as np# Load and compute returnsprices = pl.scan_csv("data/prices_daily.csv", try_parse_dates=True)returns = ( prices.sort(["Ticker", "Date"]) .with_columns([ ((pl.col("Close") / pl.col("Close").shift(1)) - 1) .over("Ticker") .alias("Return") ]) .filter(pl.col("Return").is_not_null()) .select("Return") .collect() .to_series() .to_numpy())# Histogram with normal overlayfig, ax = plt.subplots(figsize=(10, 6))ax.hist(returns, bins=50, density=True, alpha=0.7, label="Returns")mu, sigma = np.mean(returns), np.std(returns)x = np.linspace(returns.min(), returns.max(), 100)ax.plot(x, np.exp(-0.5 * ((x - mu) / sigma) ** 2) / (sigma * np.sqrt(2 * np.pi)), 'r-', linewidth=2, label="Normal fit")ax.set_xlabel("Daily Return")ax.set_ylabel("Density")ax.set_title("Returns Distribution vs Normal")ax.legend()ax.grid(True, alpha=0.3)plt.show()

Key Insights: Financial returns typically have fat tails (more extreme values than normal distribution) and slight skewness. This informs model choice—use robust methods or models that account for non-normality.

Interpretation: The mean return is close to zero (0.000471), indicating the market is roughly efficient. The standard deviation (0.010540) shows moderate volatility. The range from -3.98% to +4.07% indicates significant tail risk, confirming the fat-tailed nature of financial returns.

Feature Distributions (Multiple Assets):

# Compare return distributions across assetstickers = ["AAPL", "MSFT", "GOOGL"]returns_by_ticker = {}for ticker in tickers: ticker_returns = ( prices.filter(pl.col("Ticker") == ticker) .with_columns([ ((pl.col("Close") / pl.col("Close").shift(1)) - 1).alias("Return") ]) .select("Return") .collect() .to_series() .to_numpy() ) returns_by_ticker[ticker] = ticker_returns[~np.isnan(ticker_returns)]# Box plot comparisonfig, ax = plt.subplots(figsize=(10, 6))ax.boxplot([returns_by_ticker[t] for t in tickers], labels=tickers)ax.set_ylabel("Daily Return")ax.set_title("Return Distributions by Asset")ax.grid(True, alpha=0.3)plt.show()

Time Series Plots

Time series plots reveal trends, cycles, regime changes, and anomalies.

# Prepare time series data for visualizationdf = pl.read_csv("data/finance.csv")df_ts = df.select(['date_id', 'forward_returns']).head(200)print('Time series data summary:')print(f'Date range: {df_ts["date_id"].min()} to {df_ts["date_id"].max()}')print(f'Returns range: {df_ts["forward_returns"].min():.6f} to {df_ts["forward_returns"].max():.6f}')print(f'Mean return: {df_ts["forward_returns"].mean():.6f}')print(f'Std return: {df_ts["forward_returns"].std():.6f}')print(df_ts.head(10))

Interpretation: The time series shows daily forward returns with moderate volatility (std ~0.01). The range from -3% to +3.2% indicates typical daily market movements. Negative mean return (-0.000734) in this sample suggests a slightly bearish period.

Interpretation: forward_returns and market_forward_excess_returns are nearly perfectly correlated (0.999943), which is expected since excess returns are forward returns minus risk-free rate. The risk-free rate has minimal correlation with returns (-0.001019), consistent with market efficiency theory.

Interpretation: E7 has the most missing values (6,969 out of 9,021, ~77%), indicating this feature is unavailable for most of the time period. This pattern suggests different features become available at different times, which is common in financial datasets where new data sources are added over time.

Model Interpretation Visualization

After training models (Chapter 4), visualization helps understand predictions, identify failures, and communicate results.

Feature Importance

For tree-based models (XGBoost, LightGBM), visualize which features matter most:

import xgboost as xgb# Train model (example - see Chapter 4 for details)# model = xgb.XGBRegressor().fit(X_train, y_train)# Get feature importancefeature_importance = pd.DataFrame({ 'feature': feature_names, 'importance': model.feature_importances_}).sort_values('importance', ascending=False)# Plotfig, ax = plt.subplots(figsize=(10, 8))ax.barh(feature_importance['feature'][:20], feature_importance['importance'][:20])ax.set_xlabel("Importance")ax.set_title("Top 20 Feature Importances")ax.invert_yaxis()plt.tight_layout()plt.show()

Example (Simulated Feature Importance):

For demonstration purposes, here's a simulated feature importance analysis:

Interpretation: In this simulated example, S3 (sentiment feature) and D2 (regime feature) are the most important, together accounting for ~47% of total importance. This suggests regime and sentiment signals are key drivers of predictions.

Prediction Plots

Compare actual vs predicted values to assess model quality:

# Actual vs Predictedfig, axes = plt.subplots(2, 1, figsize=(14, 10))# Time series plotaxes[0].plot(y_test.index, y_test.values, label="Actual", alpha=0.7, linewidth=1.5)axes[0].plot(y_test.index, y_pred, label="Predicted", alpha=0.7, linewidth=1.5)axes[0].set_ylabel("Return")axes[0].set_title("Actual vs Predicted Returns")axes[0].legend()axes[0].grid(True, alpha=0.3)# Scatter plotaxes[1].scatter(y_test.values, y_pred, alpha=0.5)axes[1].plot([y_test.min(), y_test.max()], [y_test.min(), y_test.max()], 'r--', linewidth=2, label="Perfect Prediction")axes[1].set_xlabel("Actual Return")axes[1].set_ylabel("Predicted Return")axes[1].set_title("Prediction Accuracy")axes[1].legend()axes[1].grid(True, alpha=0.3)plt.tight_layout()plt.show()

Example (Simulated Predictions):

For demonstration, here's a simulated actual vs predicted comparison:

Interpretation: High correlation (0.9834) indicates the model captures the direction and magnitude of returns well. Low RMSE (0.001859) and MAE (0.001479) relative to the return standard deviation (0.010540) suggest good prediction accuracy. In practice, achieving such high correlation is challenging and requires careful feature engineering and model tuning.

Uncertainty Visualization

For probabilistic models (Chapter 4, Section 5), visualize prediction intervals:

Connection to Chapter 4: Probabilistic forecasting (Section 4-05) produces quantile predictions. These visualization patterns help communicate uncertainty to stakeholders and assess calibration.

Comprehensive Probabilistic Dashboard

For probabilistic models that predict multiple quantiles (e.g., 5th, 10th, 25th, 50th, 75th, 90th, 95th percentiles), a comprehensive dashboard provides multiple views of model performance and uncertainty. This section describes a multi-panel visualization that combines forecast accuracy, calibration assessment, risk analysis, and actionable trading signals.

1. Probabilistic Fan Chart

Purpose: Visualize prediction intervals over time with multiple confidence levels, showing both the median forecast and actual outcomes.

Components:

Confidence bands: Multiple shaded regions representing different confidence intervals (50%, 80%, 90%)

Median forecast line: The 50th percentile prediction (point forecast)

Actual values line: Observed returns for comparison

Outlier markers: Red X markers where actual values fall outside the 90% confidence interval

Interpretation:

Narrow bands: Model is confident about predictions (low uncertainty)

Wide bands: Model is uncertain (high uncertainty periods, e.g., market stress)

Actual within bands: Model's uncertainty estimates are appropriate

Many red X's: Model underestimates tail risk (confidence intervals too narrow)

Few red X's: Model captures extreme events well

Finance Insight: Wide confidence intervals during volatile periods (e.g., financial crises) indicate the model correctly identifies high-uncertainty regimes. This information is crucial for position sizing—reduce exposure when bands are wide.

2. Prediction Interval Calibration

Purpose: Assess whether the model's confidence intervals are correctly calibrated (i.e., a 90% confidence interval actually contains 90% of outcomes).

Actual coverage bars: Observed coverage rates from validation data

Color coding: Green if actual coverage is within 5% of expected, red otherwise

Interpretation:

Well-calibrated (green): Model's uncertainty estimates are reliable—when it says "90% chance," it's accurate

Overconfident (actual < expected): Model underestimates uncertainty—confidence intervals are too narrow

Underconfident (actual > expected): Model overestimates uncertainty—confidence intervals are too wide

Finance Insight: Calibration is critical for risk management. If a 5% VaR (Value at Risk) is supposed to be breached 5% of the time but is breached 10% of the time, the model is underestimating tail risk—a serious issue for portfolio risk management.

3. Probability of Positive Return

Purpose: Convert quantile predictions into a single probability metric: P(return > 0), which is directly interpretable for trading decisions.

Components:

Bar chart: Each bar shows P(return > 0) for a time period

Color coding:

Green (bullish): P > 60% (high confidence positive return)

Red (bearish): P < 40% (high confidence negative return)

P > 60%: Strong bullish signal—model predicts positive return with high confidence

P < 40%: Strong bearish signal—model predicts negative return with high confidence

P ≈ 50%: Market is efficient—no clear directional signal

Finance Insight: In efficient markets, P(return > 0) should hover around 50% most of the time. Deviations above 60% or below 40% represent rare, high-conviction signals that may warrant position adjustments.

4. Uncertainty Structure (Prediction Spread)

Purpose: Analyze the relationship between different confidence interval widths to understand uncertainty patterns.

Components:

Scatter plot: X-axis = 50% CI width (IQR), Y-axis = 90% CI width

Color mapping: Tail heaviness ratio (90% CI width / 50% CI width)

High tail heaviness (red): Extreme uncertainty in tails—model sees potential for large moves

Low tail heaviness (yellow): Uncertainty is concentrated in the middle—more normal distribution

Wide 50% CI but narrow 90% CI: Unusual pattern suggesting model inconsistency

Finance Insight: High tail heaviness indicates periods where extreme outcomes are more likely (fat-tailed distributions). This is common during market stress and should trigger risk management actions.

5. Quantile Distribution of Actuals

Purpose: Verify that actual returns fall into predicted quantile bins with expected frequencies (calibration test).

Components:

Bar chart: Frequency of actual returns falling into each quantile bin

Expected line: Theoretical distribution (5% in each tail, 15% in each quartile, 25% in each middle quartile)